F or we, to find a property concerns a down-payment and having home financing to fund all pick. When interest levels are low, consumers has actually greater buying power. However, ascending rates allow it to be much harder for consumers in order to qualify for a financial loan, especially in places where the cost of homes is continuing to grow. Solution mortgage selection should be important https://paydayloancolorado.net/basalt/ for consumers up against troubles getting mortgage loans and buying residential property. Using this type of information, buyers often most useful understand how an assumable financial works and whether or not it will be the best choice.

To own educational objectives just. Usually consult a licensed financial or mortgage elite prior to proceeding having one a house deal.

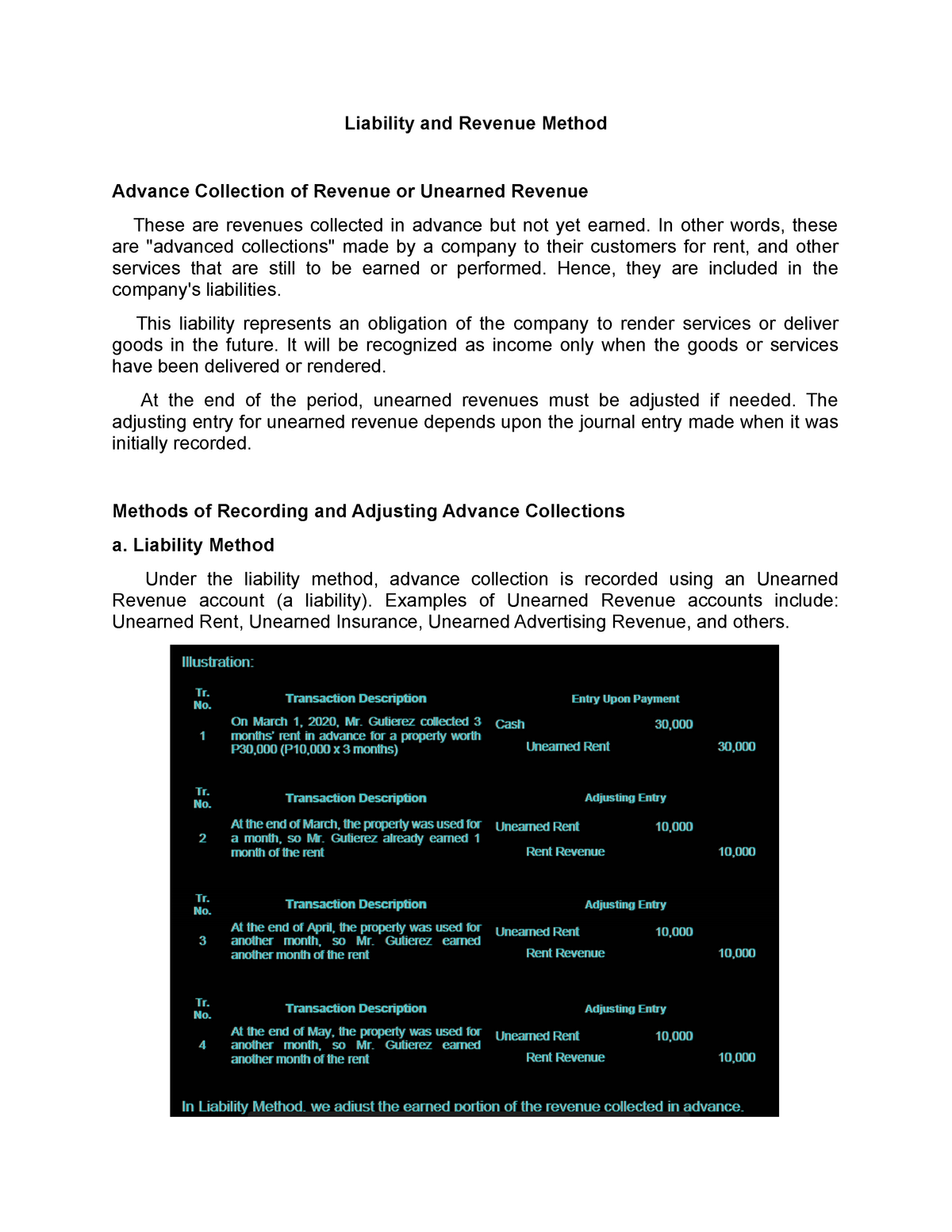

What exactly is an enthusiastic Assumable Financial?

A keen assumable home loan is a home loan that may efficiently feel transferred from just one person to another. Not absolutely all mortgage sizes enable it to be a different sort of borrower to assume the mortgage, such as for instance conventional finance. An enthusiastic assumable home loan requires the done deals of the home so you’re able to the customer. In place of getting a lump sum payment to repay the mortgage, the vendor gets involved during the a method to accept commission because of their collateral yourself and import the mortgage to another borrower.

You can find additional assumable mortgage loans, and people should comprehend the differences before you choose one to. The very first is an easy presumption, when the client agrees to really make the home loan repayments efficiently for the part of one’s supplier. The financial institution is not employed in this step, which means each other merchant and you may client remain responsible for new personal debt. This form are strange whilst requires the provider to keep the loan. Novation is yet another assumable home loan types of when the bank performs a great popular role into the determining whether the buyer is suppose the loan.

What types of Mortgages Is Assumable?

Mortgage loans you to various bodies groups guarantee normally have a clause you to lets someone to suppose the mortgage. These regulators groups tend to be:

- FHA

- USDA

- Virtual assistant

Occasionally, customers can also be suppose these mortgages without having to pay having an assessment otherwise a supplementary advance payment outside of the equity they should shell out so you can the vendor. Concurrently, these types of government-recognized finance could possibly get limit the types of settlement costs this new people are charged and also the complete count. To visualize the mortgage, people must meet the loan qualifications place by the service. For example, if in case a great Virtual assistant mortgage would need the consumer to get to know qualifications standards pertaining to armed forces services.

Old-fashioned finance usually are perhaps not assumable. In most cases, old-fashioned loans have a condition that really needs the vendor to use new proceeds of the revenue to repay the borrowed funds. Owner dont transfer home ownership to a different person in place of dropping the borrowed funds. Since the merchant needs to pay off the borrowed funds as an ingredient of the revenue, it will be impractical to policy for the customer to assume the current financial.

Advantages out-of Assumable Mortgages

- Lower interest levels

- All the way down settlement costs

- Smaller financial size

The capability to get a lowered interest with the an enthusiastic assumable financial utilizes several products, such as the types of mortgage in addition to newest mortgage rates. A person who bought or refinanced a luxury family when rates was basically reduced might have an even more affordable home loan than simply a great mortgage that an alternative consumer might get today. If mortgage you will promote much time-identity gurus along side lifetime of the loan, mostly if it’s a predetermined-speed home loan.

Even in the event borrowers which assume home financing typically have to blow an excellent huge down-payment, they could not have to shell out as often various other can cost you. Finance guaranteed by the such agencies always lay closure rates limits, normally tied to a specific buck number. In exchange for a much bigger down-payment than could be necessary getting an alternate home loan, individuals keeps an inferior loan. Such as, a debtor exactly who assumes on home financing which is 50 % of paid off may have that loan which is half the level of a another one.

Drawbacks away from Assumable Mortgage loans

- Higher off repayments, which can be possibly somewhat higher

- Fees having moving the borrowed funds

- Home loan insurance conditions

Whenever borrowers suppose a mortgage, it basically pay the seller’s down payment and collateral from the household. The new advance payment number relies on the newest mortgage’s established count and you can the fresh house’s revenue rates. In case your provider provides reduced half of good $400,000 home (including the down-payment), the customer will be expected to assembled $2 hundred,000 since the a down payment.

And the high advance payment, customers will discover that looking for an assumable home loan helps to make the home-to acquire techniques much harder. Not all the suppliers are prepared to go through the procedure of mortgage expectation, particularly when it limitations their capability to try to get the same form of financing. Vendors may predict something in return for the advantage offered to the consumer, such as a high cost. Even if and when home financing could possibly get include fewer settlement costs, it could cause a high payment per month. Assumable mortgages will often have insurance rates requirements that may not apply at conventional money.

Financial Transfer Acceptance

Quite often, consumers have to rating recognition throughout the lender prior to they are able to assume home financing. An easy expectation might be you’ll every so often, but most providers are unwilling to continue steadily to shoulder the fresh new financial responsibility into the financial. Therefore, consumers who want to assume a mortgage of someone they do perhaps not learn will likely need to use the newest station regarding novation. It means deciding the lender’s standards, distribution papers which have evidence of income, and you will waiting around for underwriting to decide a reply.

Assumable mortgages has criteria, and they may come away from multiple present. Talking about not necessarily just like the prerequisites in order to be considered to possess an alternate mortgage of the identical types of. Such as for example, a person who is applicable for a unique FHA mortgage usually should pay for an appraisal. To imagine an FHA financial, not, this new debtor may not. Loan providers usually fees charge in order to process a software to visualize an effective financial, but it age as the charges it charges for a new home loan. Homes from inside the teams with subscription charges and commitments, such apartments or gated society property, need more applications.

Search having Financial Choices

Finding the best household often begins with obtaining correct financial, and you can people might have choices they’re able to envision. Ascending interest rates convert so you’re able to diminished to buy energy, and work out assumable mortgage loans a stylish alternative. Assumable mortgages succeed consumers so you can lock in an identical words new merchant has on the borrowed funds, nevertheless they will often have and come up with a greater downpayment to get it. Considering these types of activities causes it to be more relaxing for consumers to check the solutions and decide to the mortgage choice that actually works better in their mind.

Getting informative purposes just. Usually speak with a licensed financial otherwise mortgage top-notch just before continuing having one real estate deal.